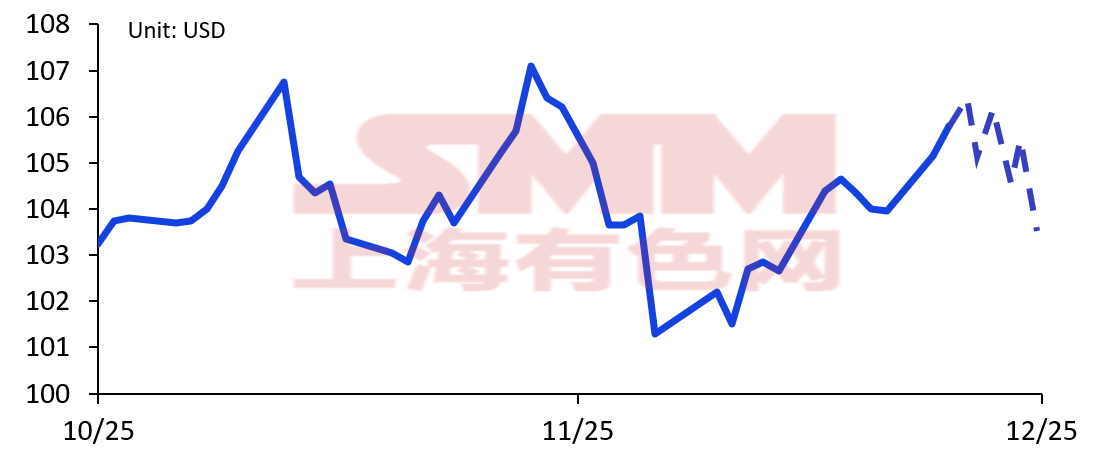

SGX Iron Ore futures Price

Sources: SGX; SMM

As of November, the SGX iron ore December futures price rebounded after a brief decline at the beginning of the month. The fluctuation in iron ore prices was mainly due to unmet market expectations regarding the reduction in hot metal output, coupled with a slight recent improvement in the fundamental supply-demand relationship.

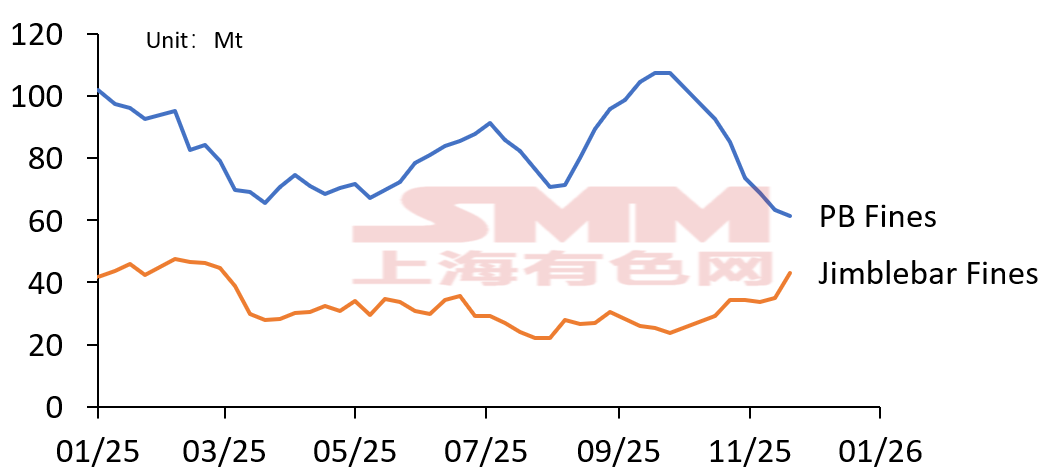

On the one hand, the restrictions on the restriction of Jimblebar Fines at some ports have objectively reduced the number of resources available for circulation in the market. Although the overall iron ore inventory is still in a state of accumulation, the structure is obviously differentiated: the inventory of PB Fines and other minerals has dropped significantly, and the spot shortage has increased. At the same time, driven by the phased rebound in molten iron production, the market trading atmosphere tended to be active, speculative buying increased, and the iron ore swap price was further pushed up.

On the other hand, the announcement on energy security during the heating season issued by the National Development and Reform Commission on November 13 suppressed the market's previous sentiment that coking coal and coke would continue to strengthen, and eased concerns about the tight supply of coking coal for steelmaking. The cooling of sentiment has provided some relief for the price of ore.

PB Fines and Jimblebar Fines Stockpile at China Ports

Sources: SMM

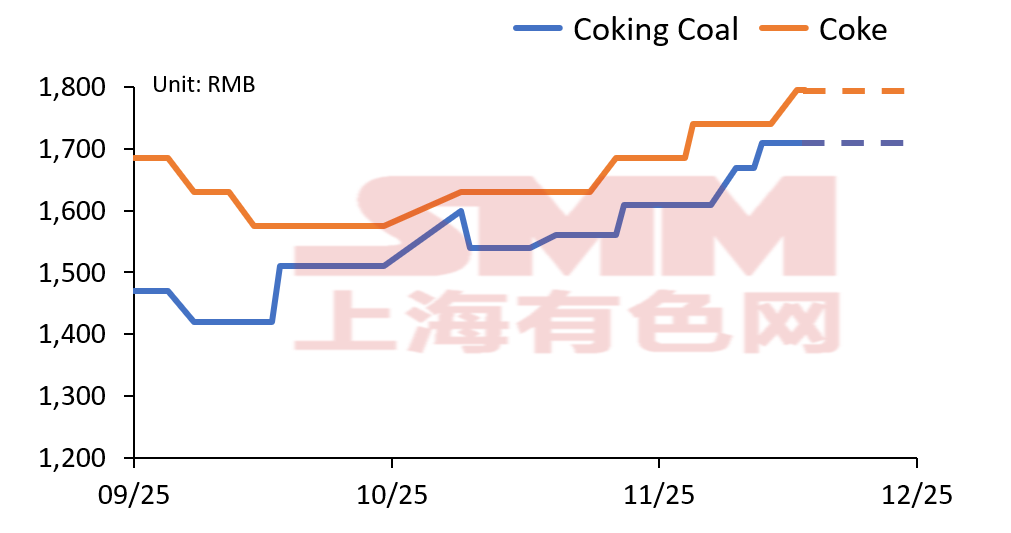

Coking coal and coke prices

Sources: SMM

But from the overall trend, the fundamentals of the current iron ore market still tend to be in a pattern of supply overing demand. As seasonal demand weakens, iron ore prices face greater resistance and support weakens. The main pressure comes from the compression of steel mill profit margins and the expectation of weak steel consumption:

SMM Hot Metal Production Forecast

Sources: SMM

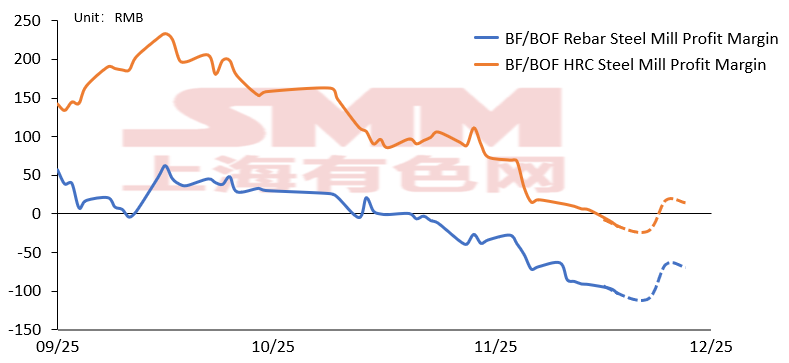

SMM Steel Plant Profit Margin

Sources: SMM

In the view of demand force, during the winter season, some regions have tightened environmental protection and production restriction policies in order to implement the requirements for the prevention and control of air pollution, resulting in varying degrees of restrictions on the transportation of raw materials such as ore and coking coal, and the cost of railway and road transportation has increased, thereby pushing up the cost of raw materials to the factory.

Prior to this, the price of coke had experienced three rounds of increases, and the fourth round of increases was also implemented recently, with a significant cumulative increase in the price of coke per tones The profit margin of steel mills has been rapidly compressed. Some long-process steel mills have turned from micro-profit to loss-making range. Although a few enterprises still maintain micro-profit, the profit level has approached the break-even point. Although the resistance to the fifth round of coke price increase is obvious, the production and operation pressure of steel mills has increased significantly.

Against the backdrop of the off-season for demand and the continuous narrowing of profits, some steel mills have begun to arrange annual maintenance and blast furnace rotation plans. However, due to reasons such as the control of the total amount of crude steel in some areas, the winter break time was postponed. This also means that the seasonal decline in molten iron production may be significantly later than in previous years.

The blast furnace operating rate still faces uncertainty in December. It is expected that the molten iron will be reduced in late December, and the expectation that the demand side of iron ore is weak is still a strong view in the market. As steel mills enter a deeper production reduction cycle, iron ore prices may be under pressure at the end of the year and enter a stage of callback window.

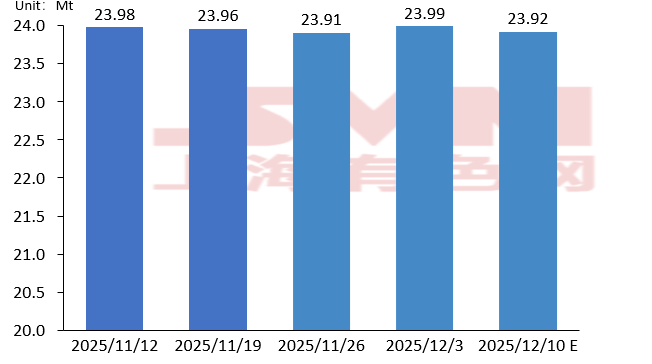

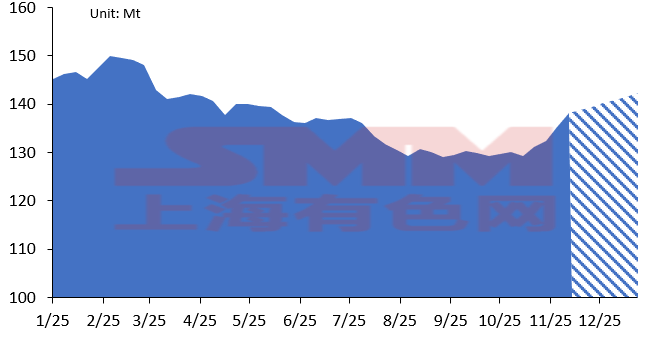

SMM Total Iron Ore Stockpile at Major Port In China

Sources: SMM

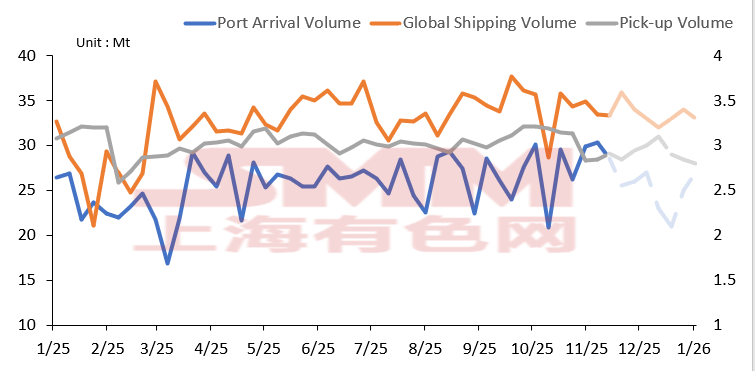

SMM Iron Ore Shipping Insights

Sources: SMM

In the context of supply force, The iron ore inventory at major port in China has re-entered a state of buildup since mid-October. Despite the customs data showed a slight MoM decline in iron ore imports in October, key indicators such as port arrival pace and global shipments suggest that mainstream supply remains steady. Rio Tinto and other major miners increased their Pilbara iron ore shipments by 5.51% QoQ in Q3, indicating continued active shipment activities in key production areas.

Restrictions on port cargo pick-up of Jimblebar fines at some ports have objectively reduced the volume of tradable resources in the market. Although overall iron ore inventory continues to accumulate, structural differentiation is evident: inventories of certain ores such as PB fines have declined notably, and spot supply tightness has increased. Meanwhile, driven by a temporary rebound in hot metal production, market trading activity has intensified, with increased speculative buying further pushing up iron ore swap prices.

From a long-term perspective, the global iron ore market is in a capacity release cycle. Multiple iron ore projects, including the Simandou iron ore project and Vale’s Capanema project, are still in the ramp-up stage, with considerable shipment capacity. Therefore, whether in the long or short term, the loose supply pattern shows no significant signs of improvement.

In summary, upside room for iron ore prices is limited. Uncertainty remains regarding steel mill production schedules and maintenance arrangements, and demand-side support for prices remains weak. Overall, iron ore prices are expected to volatile in the range of $100-110 per mt in December.

![[SMM Hot-Rolled Arrivals] Arrivals in Major Mainstream Markets Pulled Back in the First Week After the Holiday](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)